Below is a link to a CIOT guest blog by ADE Tax Principal Martin Walker

In this guest blog, Martin Walker, of ADE Tax, analyses the corporation tax rise to 25 per cent. In particular, he queries whether it will raise more money for the Exchequer, and sets out some of the likely practical implications of the increase for the UK’s tax environment over the coming years. Arguably, the impact of those changes may be to exacerbate existing distortions in the UK’s tax code and put strain on the relationship between taxpayers and HMRC.

Below is a link to Tax Journal’s feature: https://www.taxjournal.com/articles/one-minute-with-mark-bevington-

One minute with Mark Bevington, founder and principal tax adviser of ADE Tax Ltd.

What’s keeping you busy at work?

In short, transfer pricing and disputes (often together) and policy. HMRC appears to be taking some positions that are both hopeful and deeply entrenched, perhaps because it doesn’t always invest the time to properly understand the large volume of information it is now in the habit of requesting. Judging by our portfolio, there could be some ground-breaking cases decided in the next few years, especially on transfer pricing/diverted profits tax matters where parties have historically shied away from litigation and also cases relating to the extent to which complex legislation is ‘stretched’ to cover situations which might be seen as falling between the cracks of different provisions.

I also support clients in their interactions with the OECD; it is of paramount importance to make sure their multilateral proposals to reform the way profits are allocated are made to work. International tax only works with multilateral rules, but I worry that the OECD has a long way to go to understand the full implications of changing the tax system in response to the digitalisation of the economy.

If you could make one change to a tax law or practice, what would it be?

It was heartening to see a change in the recent Budget which we and others had worked hard to secure: namely, the removal of anomalies on when a business relocating to the UK could claim a deduction for goodwill amortisation.

But if I could make a further change, it would be to resolve more disputes through ‘baseball arbitration’ where the arbitrator or court has to choose one side’s position in its entirety. This would help concentrate minds on all sides. The biggest risk for many taxpayers is double taxation, and a better arbitration process is central to managing that.

Are there any new rules that are causing a particular problem?

I believe that few have thought through the true implications of moving to destination-based corporate income tax, as seen in unilateral digital taxes and the OECD’s unified approach. There is a danger that these could create perverse incentives that might harm trade and growth overall, most particularly a ‘race to the top’ in corporate income tax. Whether or not you approved of the tax competition seen in the last 15 years, this trend could significantly harm global growth.

Has a recent tax case caught your eye?

The Supreme Court decision in Fowler [2020] UKSC 22 is a well written and thought provoking judgment. It reminds me a little of Jerome v Kelly [2004] 2 All ER 835, in that, post reading, it makes you wonder why the issue seemed so complex. Fowler might be ostensibly about taxing rights of divers under a treaty but the way the court approached a difficult question is useful for any tax adviser of any specialism to study. It is also a salient reminder of the difficulty advisers face when there is a binary answer and both outcomes are sensibly arguable.

What should we look out for later this year?

The coronavirus pandemic has amplified a trend we were already seeing where countries are prepared to take positions which serve their short-term interests, even if they do collective harm in the long term. In tax, we are at a crossroads where we risk abandoning the existing international rule base without having consensus on its replacement. This should be of concern to boards of multinationals, not just their tax departments.

And finally, you might not know this about me but…

I am one of the 0.4% of the population who has an identical twin. My brother left a finance career after six months to become a teacher and is now head of a school in Norwich. Even living in different cities, people occasionally tell me off for ignoring them not realising they had encountered my brother.

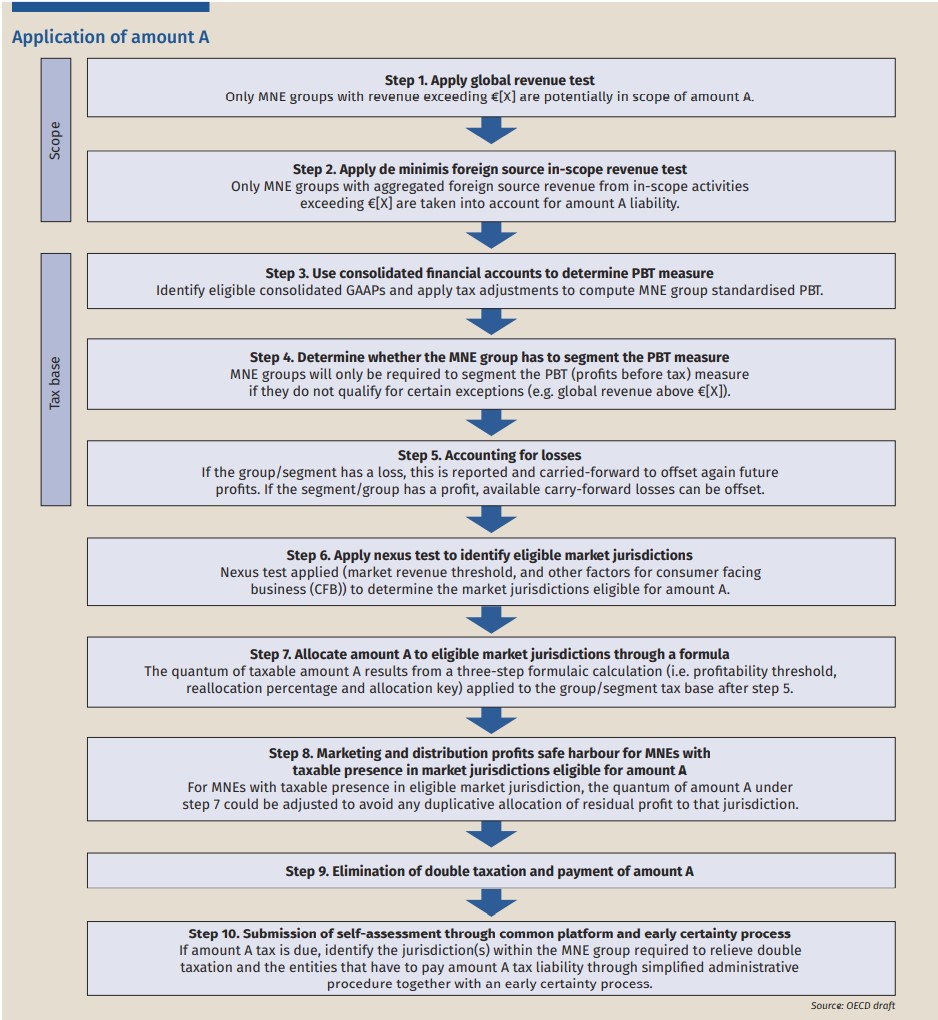

The draft OECD pillar one proposals are complex and deal with more difficulties and issues than any of us might individually imagine. The proposals envisage eleven building blocks: six for ‘amount A’ (allocating taxing rights to the market jurisdictions); two for ‘amount B’ (establishing fixed returns for marketing and distribution activities); two concerning procedures to achieve ‘tax certainty’; and a final building block covering implementation and administration. If pillar one is to be implemented, impacted groups have much to prepare for and little time to waste. However, with the US currently outside the process and complexities mounting, some might ask whether this whole journey is worth the effort.

As reported in Tax Journal (18 September 2020), leaks of the OECD’s ‘confidential’ proposals of 3 August 2020 to tax administrations have been doing the rounds of MNEs and advisory firms: 225 pages of detailed descriptions and analyses – bridging divergent interests and accommodating commercial complexities.

Eleven building blocks are identified. Six concern the new taxing right (‘amount A’), i.e. how to identify when an MNE should have an amount of residual profit reallocated among market countries; and how that should be identified, allocated and relieved. Two concern the fixed return for defined baseline marketing and distribution activities (‘amount B’), i.e. how to increase certainty on returns for ‘routine activities’. A further two relate to procedures to achieve ‘tax certainty’, and the final building block is on implementation and administration.

What, therefore, are the three Ps? Policy and Politics will ultimately determine whether pillar one comes into force. If so, the Practicalities of implementation will not be easy.

Policy

The OECD appears to have worked diligently to accommodate the widespread desire to allocate some of an MNE’s profits according to where its customers or users are. Yet important fundamental differences appear to remain. Is the purpose of amount A to ‘top up’ what a market territory is no longer generating from local activities (thanks to digitalisation) or is it a broader shift towards some taxing rights centring on the location of users

This question impacts on how residual losses might be relieved and when an amount A allocation is not required because of taxable income already in the territory.

It is one thing to justify who should receive an allocation, but quite another to determine where that same amount should be relieved and whether such relief should be by exemption or credit. This makes a real difference to whether ‘top up’ tax from a territory should be charged, and there is a further question of whether credit amount should be pooled.

The OECD appears to have listened to taxpayers’ desire for certainty; however, as mentioned below, there is a rather important catch.

Politics

There is no shrinking from the elephant in the room. Given that so many of those likely to be affected are US MNEs, can a new international system really be adopted that the US does not recognise? Many such MNEs have regional headquarters in countries that remain part of the pillar one discussions, and the regime could conceivably apply by reducing their profits (the practicalities of regional structures are dealt with in Chapter 7).

However, the fear of anomalies and injustice may be a significant barrier.

The draft may revive the nagging question of what this whole exercise is for. Put most simply, it is not clear which countries will be the losers in any reallocation

More broadly, the draft may revive the nagging question of what this whole exercise is for. Put most simply, it is not clear which countries will be the losers in any reallocation. The OECD may be banking on the expectation that countries will value the taxes reallocated to them more highly than the unilateral taxes they are giving up (as those reallocated taxes are more likely to be passed on to consumers). Countries may take positions on issues such as thresholds and allocation percentages based upon what most benefits them. There is a danger that under pillar one most countries will raise roughly the same amount of tax as before but in a highly expensive and more complex way.

Practicalities

For readers of this journal, the practicalities involved in implementing pillar one are likely to be by far the most significant issue. Such is the complexity of pillar one that it may take the combined minds of the tax profession a fair amount of time to fully hone a response. Perhaps due to this, the draft suggests the possibility of an entry threshold that will be reduced over time, meaning that only the very largest groups will fall within the regime initially. How that sits with the abolition of unilateral taxes is unclear. Some headline practical issues are set out below.

Scope/nexus

There are different rules for automated digital services (ADS) and consumer facing business (CFB). For ADS, there is a positive list of ADS activities, a negative list of non-ADS activities and a general definition. Financial services are excluded, although some are uneasy about the justifications for that decision. The specific model that companies fall into will impact how their profits are allocated, leading to further complexities around dual category or ‘bundled’ services. Impacted groups and their advisors will need to think carefully about their model, how allocation works and how that might evolve with their offering.

For CFBs, more than one party in the supply chain can have a relationship with a consumer, even if they do not transact directly with that consumer or take title to the product. Consensus is still required on what other engagement with the market is required to give sufficient nexus and whether there should be a presumption of presence above certain income thresholds. Significantly, no distinction is made between sales to businesses and to consumers where a product is sometimes used by consumers. In contrast, a distinction is made for some components where tracing the end consumer would be very difficult (for example, car tyres).

Lastly, the complexity and controversy on how to deal with pharma businesses is significant, with some heads of tax in affected groups privately pointing to a continued lack of recognition as to how markets work differently in different territories.

Sourcing

This section reads a bit more like legislation, and it brings to life the complexities associated with tracking.

For example, a location-based advert is allocated to the territory in which the user views it, whilst other adverts are based upon the user’s residence. There is significant guidance on other complex areas, such as identifying where a cloud purchaser uses services and how to deal with situations where VPNs are used.

Importantly, it is recognised that the sheer volume of transactions will require a systems and controls based approach to auditing. The increase in interactions with tax authorities may require affected companies to expand their skill sets and knowledge base in order to cope with these changes.

Tax base

There is an important discussion around the use and acceptance of different GAAPs, including whether standard adjustments are required for expenses typically disallowed and income from equity or equity accounting.

A compromise on segmented accounts has been suggested. Broadly, the proposal is to apply this to the largest groups, mainly those which already have segmented accounts. As with many of the proposals, however, the next step calls for further consideration (suggesting that it is some way off from the finished article).

The issue of losses seems to have exposed some philosophical divides. Firstly, it is not clear whether ‘a loss’ means less profit than the allocation threshold or an absolute loss. Additionally, there are questions about how long losses may be carried forward; what anti-avoidance rules are required; and whether and how to ensure parity between companies with volatile versus smooth profits.

These all reflect unresolved policy questions and give rise to uncertainty about implementation.

Allocation

A practical question exists as to which entities should be subject to the new tax. A hierarchy is proposed which starts with entities resident in territory. Tax could be charged to all profits in these entities, which might have an important knock on effect to dividend withholding tax and treasury management in some territories. A question remains unanswered as to whether amount A should be a ‘safe harbour’ for countries, allowing them to top up taxable profits, or whether it should be a pure extra amount. There are related practical questions as to whether amount B profits should or should not count.

The most major unresolved question is what level of group profitability should lead to reallocation. Data suggests that including groups with relatively low profit margins may make the largest difference to the overall amount available for reallocation. Importantly, there is a discussion on regional/jurisdictional variation, where more tax would be reallocated to jurisdictions/regions which are more profitable. Such differential allocation is seen as difficult, and the OECD is unclear about businesses operating on a regional basis.

Eliminating double taxation

If allocation seems complex, eliminating double taxation appears even more so. Numerous problems have been identified with regards to identifying the residual profit takers such as intra-group eliminations, different GAAP and different margins arising from the contrast between, say, buy/sell and licensing. A ‘four step’ approach is therefore proposed, which consists of:

the qualitative identification of the residual profit takers;

the application of ‘profitability tests’;

assessing the connection with different markets; and

pro-rata allocations where needed.

The more you look at each of these steps, the more complex they seem. Countries claiming amount A may be easier to identify than countries agreeing to relieve it. Additionally, there is the significance of the US remaining an outsider. Could some business either gain or lose from the creation or collapse of regional structures?

It is also unclear how the divide between those territories favouring an exemption regime versus a credit regime will be resolved.

Amount B

Having a pre-agreed profit for routine marketing services, which could replace thousands of broadly similar TP studies, was seen as a prize to many groups. The reality still feels quite distant with unresolved questions about how to identify and segregate activities that are included, and whether there should be different regional/industry margins. It is hard to imagine that some countries, notorious for having an inflated view of the profit that should be allocated to routine activities, will allow a significant portion of their tax base to be eroded.

Certainty

It is hard not to sympathise with the OECD, which has been sensibly championing a better dispute prevention and resolution mechanism but must also manage countries’ concerns about loss of sovereignty. There is a sensible focus on common documentation and the concept of a lead authority. Nevertheless, the reality of balancing competing countries’ interests was never going to be an easy problem to solve. The proposal for a review panel of representative tax authorities appears sensible in theory, but those authorities are each competing for their own slice of the revenue ‘pie’, so it seems optimistic to expect them to swiftly resolve what are undoubtedly complex and novel issues.

There is a sensible emphasis on prevention. After all, it is easier for countries to agree principles whilst their financial implications remain uncertain. However, anyone involved with negotiating a bilateral APA might harbour some scepticism as to whether the process will end up advancing certainty as opposed to merely bringing forward the inevitable audit. Whilst there may be sensible proposals on training and improving MAP processes, the sheer number of pages devoted to dispute prevention/ resolution tell their own story.

Those craving mandatory binding arbitration will spot the catch: the ‘innovative’ part of it is that both competent authorities who can’t agree must agree that the mechanism should be used. To many, that may not sound ‘mandatory’ at all.

And finally, the report also covers implementation issues, which will be of greater interest to legislators than users of the new provisions.

Standing back, where does this leave us?

Firstly, with a lot of new concepts and complexity. Secondly, with a dilemma. If there is still work to do and uncertainty on implementation, is it worth thinking through this complexity now? For those advising groups likely to be impacted, the answer is probably yes: there is simply too much to think about to risk falling behind. For others, though, this process may serve as more of a reminder that not every journey takes you to the destination you imagined.

Former head of operational and securities tax at Deloitte joins firm as principal

UNITED KINGDOM, LONDON 1 January 2021 ADE Tax is pleased to announce the expansion of its tax practice. Martin Walker, former head of operational and securities tax at Deloitte London, joins the firm as principal.

Mark Bevington, managing principal of ADE Tax said: “I am delighted that Martin has come aboard. He combines legal expertise with a practical commercial approach and a problem-solving mindset. He has a reputation among clients as being a trusted adviser, is fun to work with and he has a fantastic network of independent experts in key jurisdictions. He will add a new dimension to what ADE Tax offers with his insights into transactions, management of tax risk and his financial services background.”

Martin Walker said: “I was drawn to ADE Tax’s focus on providing pure and targeted expertise that enables our clients to meet their commercial goals. Our clients need responsive advisers whom they trust to give clear and commercial advice that cuts through complexity and our structure is designed to support that approach. I’m thrilled to be joining forces with ADE Tax.”

ADE Tax helps large multi-nationals simplify their decision-making in relation to the most complex and high value tax issues and promotes workable and fair tax policy making through constructive and effective engagement with national and international tax policy makers. Since formation, ADE Tax has advised on some of the most significant and complex international and UK issues facing major multi-nationals and has represented clients in UK tax tribunals and the Court of Appeal.

Martin Walker is a qualified solicitor of nearly 20 years’ standing and was formerly head of operational and securities tax at Deloitte. He provides decision and policy support for financial services and blue-chip clients on a wide range of tax issues, combining technical expertise with practical commercial experience. He was an associate at Slaughter and May and EMEA tax counsel at Citi before joining Deloitte’s financial services tax team. He is a member of the Practical Law Tax consultation board and editor of Monroe & Nock on Stamp Duties.

We thank you for the opportunity to provide comments in relation to the Blueprints published in October. ADE Tax acts for well known multi-nationals advising on the most complex international tax and transfer pricing issues. We have supported various clients in providing detailed comments and have therefore focussed this brief submission on the key points of principle.

We believe the OECD should be commended for an open and diligent consultation process which has brought to light many specific issues. With that said, it was perhaps inevitable that both the Pillar One and Pillar Two Blueprints would therefore be significantly more complex as a result of both detailed design issues and the need to balance the interests of different countries. Accordingly, we urge the OECD to apply every effort to simplify the Blueprints before they are finalized.

Pillar One

The need to simplify

We consider that much simplification can be achieved by focussing on the reasons Pillar One was proposed in the first place: it was a response to digitalisation enabling marketing, distribution and intermediation activities to be more centralised and remote from the customer location. It follows that Pillar One should be focussed on compensating for this centralisation as opposed to being a means to fundamentally reorder the international tax system.

Simplifying Amount A

For this reason, we believe that Amount A should be a means of ensuring that customer countries can bring an MNE’s taxable income up to a certain level as opposed to being a reallocation of income that adds to whatever the country’s existing taxing rights are. This approach is optimal on both a

policy and practicality level. It is the purest means of addressing the issue Pillar One was intended to solve and also removes the need for Amount B.

Is Amount B required?

With regard to Amount B, we were among those advocating for a mechanism to fix the profit for routine distribution functions. Our thinking was that it had the potential to eliminate thousands of similar transfer pricing studies all arriving at broadly the same answer. However, in the cold light of day, we believe that the Amount B proposals will significantly complicate matters resulting in increased and more complex disputes. This is because countries will be motivated to contend that not all of an MNE’s in-country activities fall within the ‘routine’ (and therefore fixed) bucket. The result is likely to be disputes on which activities fall within or outside and then a further dispute on the profit attributable to every permutation of ‘non-routine’ activities which is tenably arguable.

We therefore urge the OECD to finalise the rules in a way that ensures distribution profits taxed by countries under traditional rules reduce their entitlement to Amount A. This reduces the incentive for dispute as to the nature of those distribution activities and their reward and therefore reduces (or perhaps eliminates) the problem that Amount B was intended to solve.

Dispute resolution

Such simplification also reduces the inherent risk of disputes arising and this is critical in view of the careful balancing act the OECD has been required to undertake. Whilst we understand countries’ concerns over sovereignty, it must be recognised that mandatory binding arbitration is the only means of eliminating double tax. If that remains politically unacceptable, we urge the OECD to recognise the resulting necessity to dramatically simplify the proposals so that the risk of such disputes is minimised.

Pillar Two

The Pillar Two Blueprint has the ambitious goal of ensuring a level playing field globally for taxpayers with international operations by imposing a global minimum tax charge. Whether such an imposition should be made upon countries is a political question upon which we have no comment. However, it is inevitable that such a broad-ranging proposal will need refining through further work, clarification and – wherever possible – simplification in order to be workable for multi-national entities. We set out below our key questions and recommendations.

Policy goal

Before further work is undertaken in refining these complex rules, we believe it is worth questioning whether or not the concerns that gave rise to the perceived need for Pillar 2 have not already been addressed by the BEPS process and US tax reform. We question whether it really is still the case that substantial profits are concentrated in jurisdictions with little substance and low tax rates. There is a widespread perception that the BEPS problem targeted US multi-nationals the most and we note that the introduction of GILTI in the US (as part of broader tax reform) means that few profits remain untaxed.

We believe that a robust re-examination of the profits which might really be taxed as a result of Pillar 2 should be undertaken since there is a risk that MNEs and tax authorities will end up complying with highly complex rules which may make very little actual difference.

The GLoBE rules: Income inclusion rule (IIR), undertaxed payments rule (UTPR) and switch over rule (SOR)

As the Pillar Two Blueprint involves granting jurisdictions new taxing rights in addition to those currently in existence in accordance with international tax standards based upon residence or permanent establishments, there is clearly a need for a universal approach. We urge the OECD members to strive towards a consistent and homogenous interpretation of these new taxing rights to limit incidences of double or even triple taxation wherever possible.

The application of the IRR to the parent entity jurisdiction and the UTPR to other group entities will require extensive statutory changes and amendments to double tax treaties. We would caution against rushing to a final set of proposals without both clear political buy-in across a wide range of participating OECD member countries and a firm plan for simultaneous implementation of taxing rights on a homogenous basis to avoid asymmetric tax treatment and/or a staggered approach across a range of effective dates (as has been the case with the current multi-lateral instrument).

In order for the IIR to function as planned, as well as the complementary proposals of the UTPR and the SOR, we consider that the following should be enshrined in the Pillar Two Blueprint:

the inclusion in the Pillar Two tax base of any unilaterally imposed gross taxes on digital services in order to avoid double or even triple taxation of the same income;

full inclusion of taxes paid under the STTR in the GLoBE rules;

full creditability of Pillar One taxes against the Pillar Two tax base (as well as further clarification of how the two Pillars interact); and

full flexibility to carry forward any ‘excess’ taxes to future years.

Coordination with tax rules such as GILTI

Clearly, coordination is needed between these proposed new Pillar Two Blueprint rules and the US GILTI regime (or any equivalent regime). Amounts taxed under GILTI should be recognised for the purposes of the Pillar Two Blueprint and further work should be undertaken so that the US base erosion and anti-abuse tax (BEAT) should not apply to payments to entities which are subject to the income inclusion rule (see below). Groups with US parent entities or intermediary holding companies will need to undertake further analysis in order to assess the impact of the Pillar Two Blueprint and further clarification will be required in order to undertake this analysis. Whilst acknowledging the political difficulties, there is a need for the US rules to fit seamlessly within the

Pillar Two Blueprint for the Blueprint to be workable, which may involve give and take on both sides.

Interaction with BEPS rules

There is a danger that amounts disallowed under anti-hybrid or interest restriction rules might still be caught by the GLoBE rules thereby causing double taxation.

Subject to tax rule (STTR)

We query whether applying taxation at source to gross payments should apply in priority to the IIR and UTPR, especially where the global effective tax rate is above the stipulated minimum tax rate. Any amounts taxed under an IRR, including the US GILTI if treated as a qualifying IRR, are not relieved by tax levied at source under the STTR. At a minimum, the amount of any tax paid under the STTR should be taken into account in the overall IIR calculation, with amounts being available to carry forward where applicable.

Where the recipient is subject to tax on amounts other than income or a specific tax regime applies, such as under a particular intellectual property regime, this could result in the application of the STTR in circumstances where its imposition does not seem to be warranted from a policy perspective. Further work seems to be required in this respect.

The need to simplify

We encourage greater simplification to the Pillar Two Blueprint wherever possible in order to ensure that each of the rules is workable on a realistic commercial basis, which will involve further work by the OECD over the coming months.

In addition to the points we have already made in this submission, we support the following as means of simplifying the compliance burden:

use of existing country by country reporting (CbCR) data wherever possible;

use of consolidated financial statements, but with flexibility to accommodate permanent and temporary differences without any adverse tax impact;

ability to blend high and low taxed income when calculating the global effective tax rate; and

publication of a list of jurisdictions annually (and before the specified effective date) in which the tax base and rate are considered to be at least aligned with the GLoBE tax base and rate. This would enable taxpayers which only operate in the specified jurisdictions to be deemed to be compliant and reduce the compliance burden.

Concluding remarks

We thank the OECD for the opportunity to comment and hope that our input is of use.

Have you experienced that time, often many months or years (and documents) into a tax dispute when you feel you’re no further forward than day one? Sometimes further back in fact; the underlying issue remains, now saddled by mutual disappointment, frustration and entrenchment. Worse still, unity among stakeholders may be lost.

That’s when a reality check’s required. Will one more attempt help the taxman see the light? More likely, mutual creativity has failed to circumvent an issue which will never be agreed. And walking away means paying the assessment; unthinkable if you believe you’re right.

‘Rightness’ may actually be the problem. Which official wants to concede if they can kick the can down the road instead? The power of Litigation is to re-frame their question. ‘Why should I concede?’ becomes ‘Do I want to lose in court?’ Often this gives a very different answer.

Offshore Receipts in Respect of Intangible Property. Or ‘ORRIP’: the UK’s bold assertion of a right to tax anywhere.

ORRIP’s rationale invites sympathy. Some central trading hub jurisdictions still allow royalties to be ‘stripped’ to offshore havens – a legacy of US tax rules that incentivised the offshore holding of US developed intangibles. If such royalties relate to UK sales, why shouldn’t the UK tax them? Is it wrong to incentivise companies to own and tax intangibles where they’re developed?

However, there are problems. Ambiguous legislation invites debate on whether outright transfers are taxed. If so, ORRIP incentivises against behaviour change it should encourage. ORRIP is also levied on gross income yet global tax reform should skinny haven’s profits to a routine capital return.

Which takes us back to principles. Through impatience to see multi-nationals comply with reformed global rules, the UK is prepared to break them. Shouldn’t rules be for everyone?

In tax, what was in the minds of decision makers can matter.

Yet a request by evidence-hungry authorities for e-mail correspondence can be

bad news. What to do? They are often relevant but how often does their

provision actually help resolve a dispute?

Their unstructured and voluminous nature often means they

obscure, not clarify, and make matters far worse if each side cherry-picks ‘helpful’

quotes. A potential hearing which turns on thousands of e-mails can force

taxpayers to accept an outcome they know isn’t fair.

The alternative? Tell your story first and tell

it well. The best accompanying analysis allows the whole story to be more

robustly, objectively and succinctly told, vastly improving protection against

cheap shots. Amazing tools exist but are unused by many. It may take effort and

skill to use them productively but it’s effort worth spending if you want your

documents to prove anything.

Like it or not, India’s proposed revisions to PE profit

attribution (https://incometaxindia.gov.in/Lists/Latest%20News/DispForm.aspx?ID=306)

require serious attention. Profit apportionment is ‘formulary’ – it starts with

India’s share of the higher of operating margin/2% allocated to India by equal

reference to Indian assets, employees and sales. Users are an extra factor for

digital companies with a 10%/20% weighting depending on intensity. So profits

are shared but not losses.

A formulary approach makes sense to many. Yet, each

uncertain input breeds and multiplies uncertainty. India’s proposals require

determination of assets and employees outside India present ‘in respect of’

Indian operations, whatever that means. Is this the path to less dispute? For

many, it will seem like a more certain path to double tax.

Hence a bigger lesson: the need to support OECD

leadership towards a unified approach. If India’s approach is unpalatable,

managing a different approach for every market territory is unthinkable.